You could be eligible for up to 50% of your spouse's benefit—or 100% if they pass away

By David Haertzen, Founder of SocialSecurityMedicare.com

Hello, friends. When we talk about Social Security, we often think of it as an individual benefit—a reward for our own years of hard work. But that's only half the story. From my decades in the insurance and financial world, I've learned that the most robust plans are built on partnership. Social Security was designed with this in mind. It's not just a program for individuals; it's a program for families.

Many couples are completely unaware that there are powerful benefits available to them based on their spouse's work record. These aren't loopholes; they are core features of the system designed to support couples and provide a critical safety net for a surviving spouse. My goal today is to pull back the curtain on spousal and survivor benefits. Understanding these rules is essential for making a coordinated claiming decision that maximizes your household income and protects your family's financial future for decades to come.

Please Note: This article is for educational purposes and is not financial advice. The rules can be complex and your situation is unique. It's crucial to get your personalized information from the official Social Security Administration (SSA) website and consider consulting an independent financial advisor.

Spousal Benefits: A Boost for the Team

A spousal benefit allows an individual to receive benefits based on their spouse's work record rather than their own. This is especially valuable in situations where one spouse was the primary breadwinner or earned significantly more over their career.

How It Works: The 50% Rule

The fundamental rule is this: you may be eligible to receive an amount that is up to 50% of your spouse's full retirement age (FRA) benefit.

To qualify for spousal benefits, a few conditions must be met:

- Your spouse must have already filed for and started receiving their own retirement benefits.

- You must be at least 62 years old.

- You must have been married for at least one year.

It's important to understand the "deemed filing" rule. When you apply for Social Security, the SSA will automatically give you the higher of your two available benefits: either the benefit based on your own work record or the spousal benefit based on your partner's record. You can't, for instance, take a spousal benefit now and switch to your own (larger) benefit later. You get one or the other—whichever is greater.

A Simple Example:

- Let's say Robert's benefit at his Full Retirement Age (FRA) is $2,800/month.

- His wife, Susan, has a smaller benefit of $800/month at her FRA.

- The spousal benefit Susan is eligible for is up to 50% of Robert's FRA benefit, which is $1,400 ($2,800 x 0.50).

- Since $1,400 is greater than her own $800 benefit, Susan's monthly check will be "topped up" to $1,400 once Robert files and she reaches her own FRA.

A quick note on timing: If you claim this spousal benefit before your own Full Retirement Age, the amount will be permanently reduced.

Survivor Benefits: A Financial Lifeline and a Lasting Legacy

Losing a spouse is one of life's most difficult experiences. Amid the grief, financial worries should be the last thing on your mind. Survivor benefits are a core part of Social Security's promise, designed to provide a continuing stream of income for the widowed spouse.

How It Works: The 100% Rule

The rule here is even more powerful: as a surviving spouse, you may be eligible for up to 100% of the benefit your deceased spouse was receiving.

This is where the claiming decision of the higher-earning spouse becomes an act of profound financial care. If the higher earner delayed their benefit until age 70, they didn't just maximize their own check—they maximized the potential survivor benefit for their partner. They've essentially locked in a larger, lifelong income stream for their spouse in their absence.

Key points for survivor benefits:

- You can claim survivor benefits as early as age 60 (or 50 if you are disabled).

- However, claiming before your Full Retirement Age will result in a reduced benefit. To receive the full 100%, you must wait until your FRA.

- Unlike with spousal benefits, you have more flexibility. For example, a widow could choose to take a survivor benefit first, while letting her own retirement benefit continue to grow until age 70, and then switch to her own larger benefit. This requires careful planning.

Spousal vs. Survivor Benefits at a Glance

This chart highlights the key difference between the two types of family benefits available through Social Security.

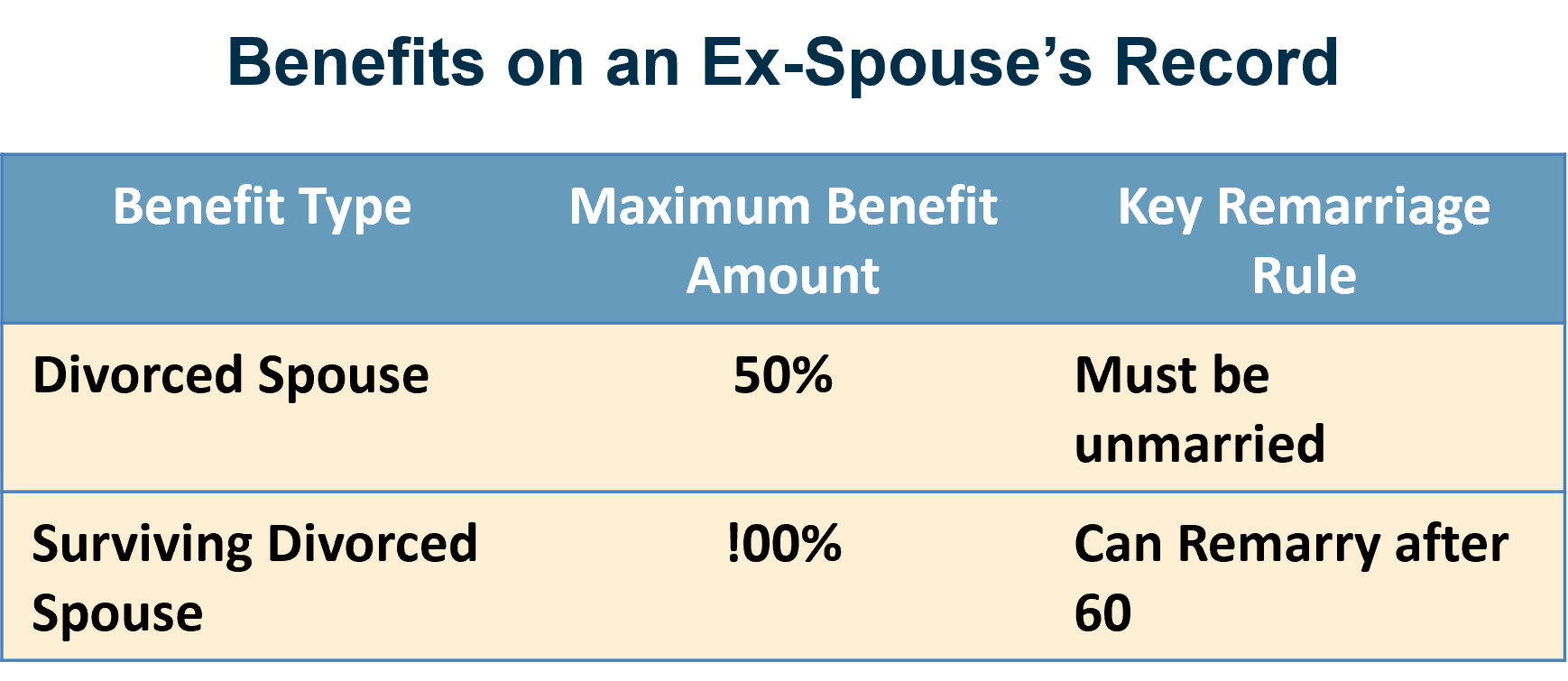

The Divorced Spouse: A Commonly Overlooked Benefit

Many people are shocked to learn that you may be able to claim benefits on an ex-spouse's record. The rules are very specific, but if you qualify, it can be a significant financial resource.

You may be eligible for spousal or even survivor benefits from an ex-spouse if:

- You were married for 10 years or longer.

- You are currently unmarried.

- You are age 62 or older.

Crucially, your decision to claim benefits has absolutely no impact on your ex-spouse's benefits or those of their current spouse. They will never even be notified. This is not about taking money from them; it's a separate entitlement you have earned by virtue of the long-term marriage.

Divorced Spouse Benefits

This chart highlights the key Divorced Spouse Benefits.

The Takeaway: Plan as a Team

Your Social Security claiming decision should be a conversation, not a solo act. For most couples, the most powerful and protective strategy is for the higher-earning spouse to delay their benefit for as long as possible, ideally to age 70. This accomplishes two critical goals: it maximizes the income you share together and it provides the largest possible safety net for the surviving spouse.

Take the time to go to the SSA Website, look at your combined statements, and talk through the options. By understanding how spousal and survivor benefits work, you can transform your individual benefits into a coordinated plan that strengthens your financial security for life.