Headlines scream about an empty trust fund.

By David Haertzen, Founder of SocialSecurityMedicare.com

Hello, friends. It’s impossible to read about retirement without seeing a scary headline: "Social Security to Run Out of Money!" "Trust Fund Will Be Depleted!" "Is Social Security Going Bankrupt?" These phrases are designed to grab your attention and, frankly, to scare you. They paint a picture of a system on the brink of collapse, where the benefits we've all worked for and paid into will simply vanish.

Let me be direct: that picture is false. As someone who has spent a career analyzing complex systems and managing risk, I can tell you that while Social Security faces a genuine financial challenge, it is absolutely not going bankrupt. The fear-mongering you hear is a fundamental misunderstanding—or misrepresentation—of how the system works. My goal today is to cut through that noise, replace fear with facts, and show you why you can and should count on receiving your Social Security check for the rest of your life.

Please Note: This article is for educational purposes only and is not financial advice. The goal is to provide clarity on a complex topic. For the official, detailed projections, you should always refer to the Social Security Administration's own reports, which you can find on the official SSA website.

Myth #1: Social Security is a Giant Bank Account (and It's Going Empty)

The biggest source of confusion comes from thinking of Social Security like a personal savings account. The reality is quite different. Social Security is a "pay-as-you-go" system. This means the contributions from today's workers and their employers are used to pay the benefits for today's retirees and other beneficiaries.

So, what about the famous "Trust Funds"? Think of them not as a savings account, but as a reservoir or a buffer. For many years, the system collected more in taxes than it paid out in benefits. This surplus was invested in special U.S. Treasury bonds, creating the Trust Funds. Now, as more Baby Boomers retire, the system is paying out more than it collects each year. It has begun drawing from that reservoir to make up the difference, ensuring full benefits are paid.

The headlines you see are about the date when that reservoir is projected to run dry (currently projected for the mid-2030s). And that sounds terrifying, until you understand what happens next.

The Real Story: A Projected Shortfall, Not a Collapse

Here is the single most important fact you need to know: even if the Trust Funds were completely depleted, Social Security could still pay a substantial portion of promised benefits.

Why? Because the "pay-as-you-go" nature of the system continues. Millions of people will still be working and paying Social Security taxes into the system every single day. The Social Security Administration's own actuaries project that even if Congress does absolutely nothing, ongoing tax revenues would still be enough to cover around 80% of promised benefits.

Let me repeat that for emphasis: The worst-case, "do-nothing" scenario is not zero benefits. It is a reduction in benefits. While a 20% cut would be painful and unacceptable, it is a universe away from the "bankruptcy" and "total collapse" that headlines suggest.

This reveals the true nature of the problem. It is not a four-alarm fire; it is a long-term, predictable, and entirely solvable accounting challenge.

A Solvable Puzzle: How We've Fixed This Before and Will Again

This isn't the first time Social Security has faced a financial crossroads. Back in 1983, the system was much closer to a genuine crisis. What happened? A Republican president (Ronald Reagan) and a Democratic Speaker of the House (Tip O'Neill) came together and made a series of modest adjustments to ensure solvency for decades to come. History has shown us that when push comes to shove, Congress always acts to protect Social Security.

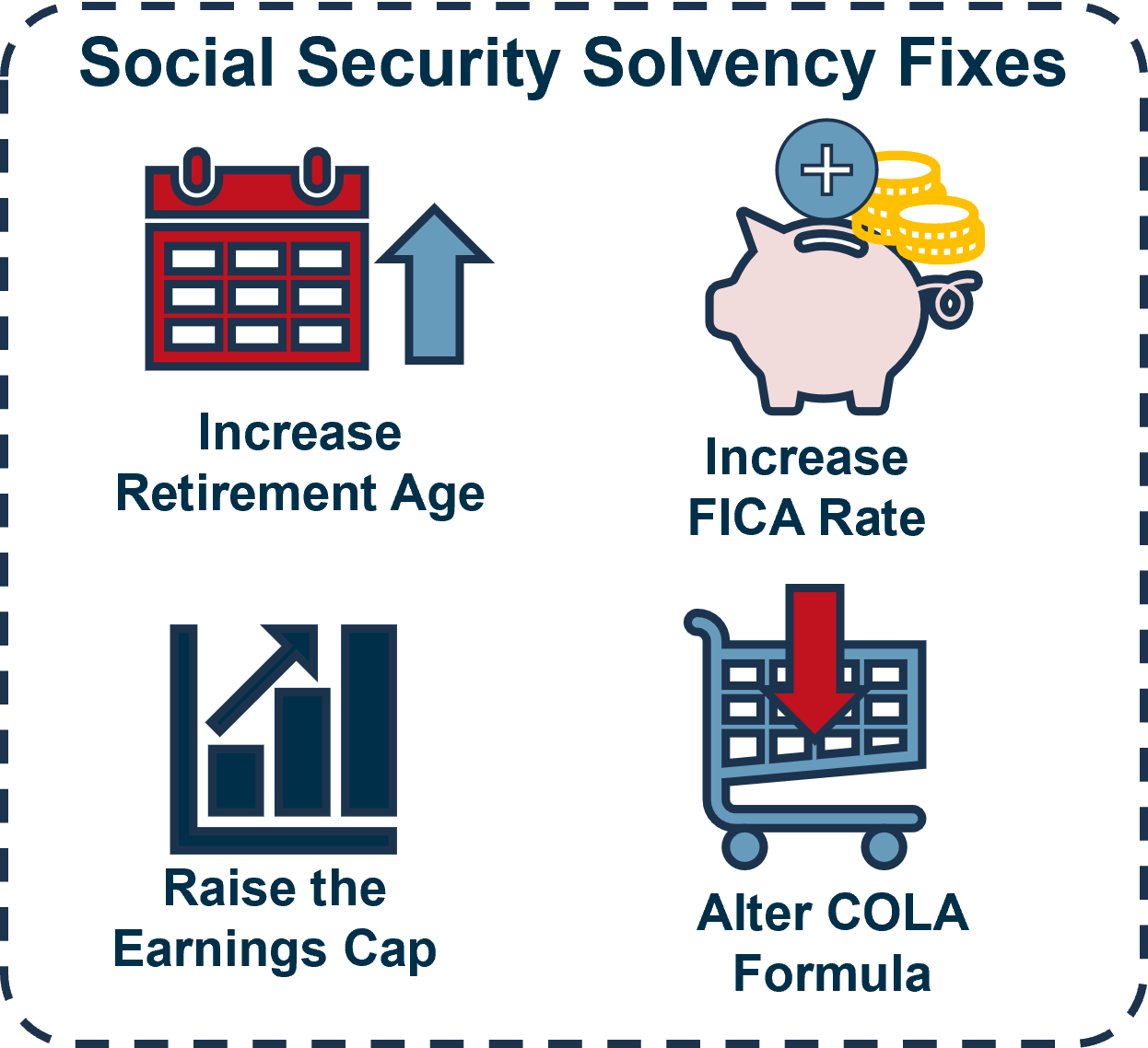

There are several well-understood "levers" they can pull to close the projected gap. The final solution will likely be a combination of a few of these small tweaks:

- Slightly Raise the Full Retirement Age: Because people are living longer, the FRA could be gradually increased for younger generations (e.g., to 68 or 69 over many decades).

- Modestly Increase the Payroll Tax Rate: The current rate is 6.2% for employees and employers. A small increase, phased in over time, would significantly boost revenue. For example, raising it by 1% over 20 years.

- Adjust the Cost-of-Living-Adjustment (COLA) Formula: Some economists argue that the current formula, based on the CPI-W, overstates inflation for retirees. Switching to a different index, like the Chained CPI, would result in slightly smaller annual raises. You can learn more about the current COLA at the SSA's COLA page.

- Raise the Cap on Taxable Earnings: In 2025, Social Security taxes are only paid on income up to a certain limit ($168,600 in 2024, it adjusts annually). Raising or eliminating this cap would mean higher earners contribute more, significantly closing the funding gap.

Multiple options with tradeoffs are on the table.

What This All Means for Your Retirement Check

So, let's bring this back to the most important question: Will you get your Social Security check?

Yes, you will.

The system is not collapsing. It has a manageable, long-term shortfall that can be fixed with minor adjustments, just as it has been fixed before. The political will to act will grow stronger as the deadline approaches, and it is overwhelmingly likely that any changes will be phased in gradually and will primarily affect younger workers, not those in or near retirement.

You have spent your entire working life paying into this system. It is a promise, a social contract. While it's wise to be informed, it is counterproductive to let fear-based headlines derail your retirement planning. Build your financial plan with the confident assumption that Social Security will be there for you. It is the most successful social program in our nation's history, and it will continue to be the bedrock of retirement security for generations to come.