Your claiming decision is irreversible and could be the most important financial choice you make for retirement. Let's get it right.

By David Haertzen, Founder of SocialSecurityMedicare.com

Hello, friends. Of all the financial puzzles we have to solve in retirement, there is one decision that stands out for its sheer, irreversible importance: choosing when to claim your Social Security benefits. This isn't just a small detail; it can be a six-figure decision that will impact your financial security—and potentially your spouse's—for the rest of your lives.

When my wife and I faced this choice, I spent countless hours running the numbers, drawing on my decades of experience in the insurance industry. We ultimately decided to wait until age 70, but that was our solution to our specific puzzle. There is no single "magic" age that is right for everyone. My goal today isn't to tell you what to do. It's to give you the clear, unbiased information and the framework you need to solve this puzzle for yourself, so you can make a confident choice that you'll be happy with for decades to come.

Please Note: This article is for educational purposes only and does not constitute financial or legal advice. Your situation is unique. Always perform your own research and consider consulting with a qualified, independent financial professional. For official social security information and to see your personal benefit estimates, visit the Social Security Administration (SSA) website.

The Three Critical Milestones: 62, FRA, and 70

The entire Social Security claiming decision revolves around three key ages. Understanding the trade-offs between them is the foundation of a smart strategy.

Age 62: The Earliest Opportunity

You can start receiving Social Security retirement benefits as early as age 62. The appeal is obvious: you get your money sooner. However, there's a significant catch. If you claim before your Full Retirement Age, your monthly benefit is permanently reduced. For someone whose Full Retirement Age is 67, claiming at 62 means receiving only about 70% of their full benefit. While you get more checks over your lifetime, each check will be smaller forever.

Your Full Retirement Age (FRA): The Baseline

Your Full Retirement Age is the age at which you are entitled to 100% of the benefit you've earned over your working career. Your FRA is determined by the year you were born:

- Born 1943-1954: FRA is 66

- Born 1955: FRA is 66 and 2 months

- Born 1956: FRA is 66 and 4 months

- Born 1957: FRA is 66 and 6 months

- Born 1958: FRA is 66 and 8 months

- Born 1959: FRA is 66 and 10 months

- Born 1960 or later: FRA is 67

Think of FRA as the neutral point. Claiming earlier results in a reduction; waiting longer results in a bonus.

Age 70: The Maximum Payout

For every year you delay claiming Social Security past your FRA, the government gives you a bonus called "Delayed Retirement Credits." These credits increase your monthly benefit by about 8% per year. This continues until age 70, at which point there is no further benefit to waiting. For someone with an FRA of 67, waiting until 70 results in a monthly check that is 124% of their full benefit amount. That's a 24% raise for life, just for waiting three years!

Visualizing the Financial Impact of Your Choice

This chart clearly shows how waiting to claim can significantly increase your monthly retirement income.

The Four Factors That Drive YOUR Decision

So, which age is right? The answer depends entirely on your personal circumstances. Let's walk through the most important factors to consider.

1. Your Health and Longevity

This is the most straightforward factor. Social Security is longevity insurance. The longer you live, the more valuable waiting becomes. If you are in excellent health and have a family history of living well into your 80s or 90s, delaying your claim is likely to result in much higher lifetime benefits. Conversely, if you have serious health conditions, claiming earlier may be the more sensible choice.

2. Your Financial Needs and Work Status

Do you need the income now to pay your bills? If you don't have other sources of income like a pension or savings, you may have no choice but to claim early. However, if you are still working or have other resources, you have the flexibility to wait. Keep in mind that if you claim before your FRA and continue to work, your benefits may be temporarily reduced by the Social Security earnings test.

3. Your Marital Status: A Legacy Decision

For married couples, this decision is not just about you—it's about protecting your partner. When one spouse passes away, the surviving spouse is entitled to receive the higher of the two Social Security benefits. If the higher-earning spouse delays claiming until age 70, they are not just increasing their own check; they are locking in a much larger survivor benefit for their partner. This can be one of the most powerful and loving acts of financial planning a couple can undertake.

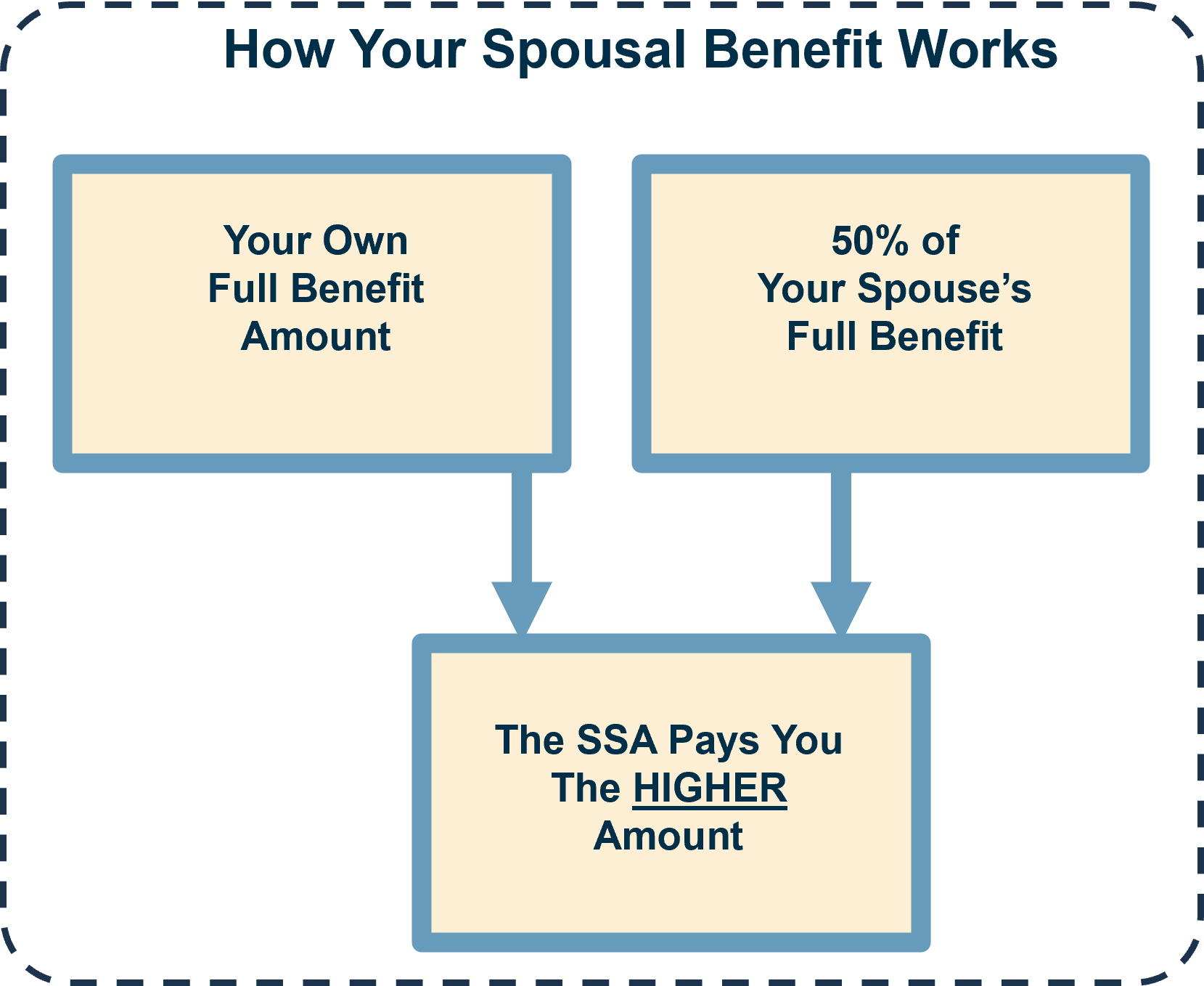

How Your Decision Affects Your Spouse

Understanding these rules is essential for couples to maximize their combined lifetime income and provide for the surviving spouse.

Making Your Educated Choice

There is no substitute for doing your own homework. The first step is to create an account at My Social Security to see your personalized earnings record and benefit estimates at different ages. Once you have your numbers, you can apply this framework:

- Consider Claiming Early (62-FRA) if: You have significant health concerns, you absolutely need the income to live, or you are coordinating a strategy with your spouse.

- Consider Claiming at FRA if: You are ready to retire, want 100% of your benefit, and don't need the income earlier.

- Consider Delaying (FRA-70) if: You are in good health, have other income to live on, and want to maximize your lifetime benefit and provide the largest possible survivor benefit for your spouse.

This is a decision that deserves your time and attention. By thinking through these factors, you can move from a place of confusion to a place of confidence, knowing you've made the best possible choice for your secure retirement.