The Social Security Earnings Test: Don't Let it Wreck Your Retirement Paycheck

By David Haertzen, Founder of SocialSecurityMedicare.com

Hello, friends. For many of us, retirement isn't a hard stop. It's a gradual transition. We might leave a long-term career to work part-time in a field we're passionate about, start a small consulting business, or simply pick up a job to stay active and supplement our income. The idea of earning a paycheck while also collecting the Social Security benefits we've worked for our whole lives sounds like a perfect combination.

But this is where many retirees get a nasty surprise. They start working, their first Social Security checks arrive, and then suddenly they receive a letter from the government saying their benefits are being reduced. This is due to a rule called the "Social Security Earnings Test," and it's one of the most misunderstood parts of the entire system. My goal today is to demystify this rule completely. We'll turn it from a source of fear into a simple, predictable part of your financial plan, so you can work and retire on your own terms, without any unwelcome surprises.

Please Note: This article is for educational purposes only and is not financial advice. The numbers used are for illustration and change annually. For the most up-to-date earnings limits and official information, please visit the Social Security Administration's official page on the topic.

The Single Most Important Rule: It's All About Your Age

Before we get into any numbers, let me give you the most critical piece of information about the earnings test: it only applies if you are collecting Social Security benefits AND you are younger than your Full Retirement Age (FRA).

That’s it. Once you reach your Full Retirement Age (which is 66 or 67 for most people today), the earnings test vanishes completely. You can earn a million dollars a year and your Social Security benefit will not be reduced by one penny. This is a key reason why delaying your benefits can simplify your financial life, but we'll get to that later.

For now, just remember: if you are under your FRA, you need to know these rules. If you're at or over your FRA, you can file this information away for your friends and family.

How the Earnings Test Works: The Two Tiers

The test operates on two different levels, depending on how close you are to your Full Retirement Age.

Tier 1: For the Years *Before* You Reach FRA

If you are collecting benefits and are, for the entire year, younger than your FRA, a specific limit applies. In 2025, that limit is $23,400. (This number is adjusted for inflation each year).

The Rule: For every $2 you earn *above* that annual limit, the Social Security Administration (SSA) will temporarily withhold $1 of your benefits.

Simple Example: Let's say your annual earnings limit is $23,40 and you take a part-time job where you earn $26,320 for the year.

- You have earned $4,000 over the limit ($27,400 - $23,400).

- The SSA will withhold $1 for every $2, so they will hold back $2,000 of your benefits ($4,000 ÷ 2).

Tier 2: For the Year You *Reach* FRA

In the year you will reach your Full Retirement Age, the rules become much more generous. A higher earnings limit applies, and it only counts the earnings you make in the months *before* the month you reach FRA.

In 2025, that higher limit is $62,160.

The Rule: For every $3 you earn *above* this higher limit, the SSA will temporarily withhold $1 of your benefits.

Once the calendar flips to the month of your birthday, the test disappears completely for the rest of your life.

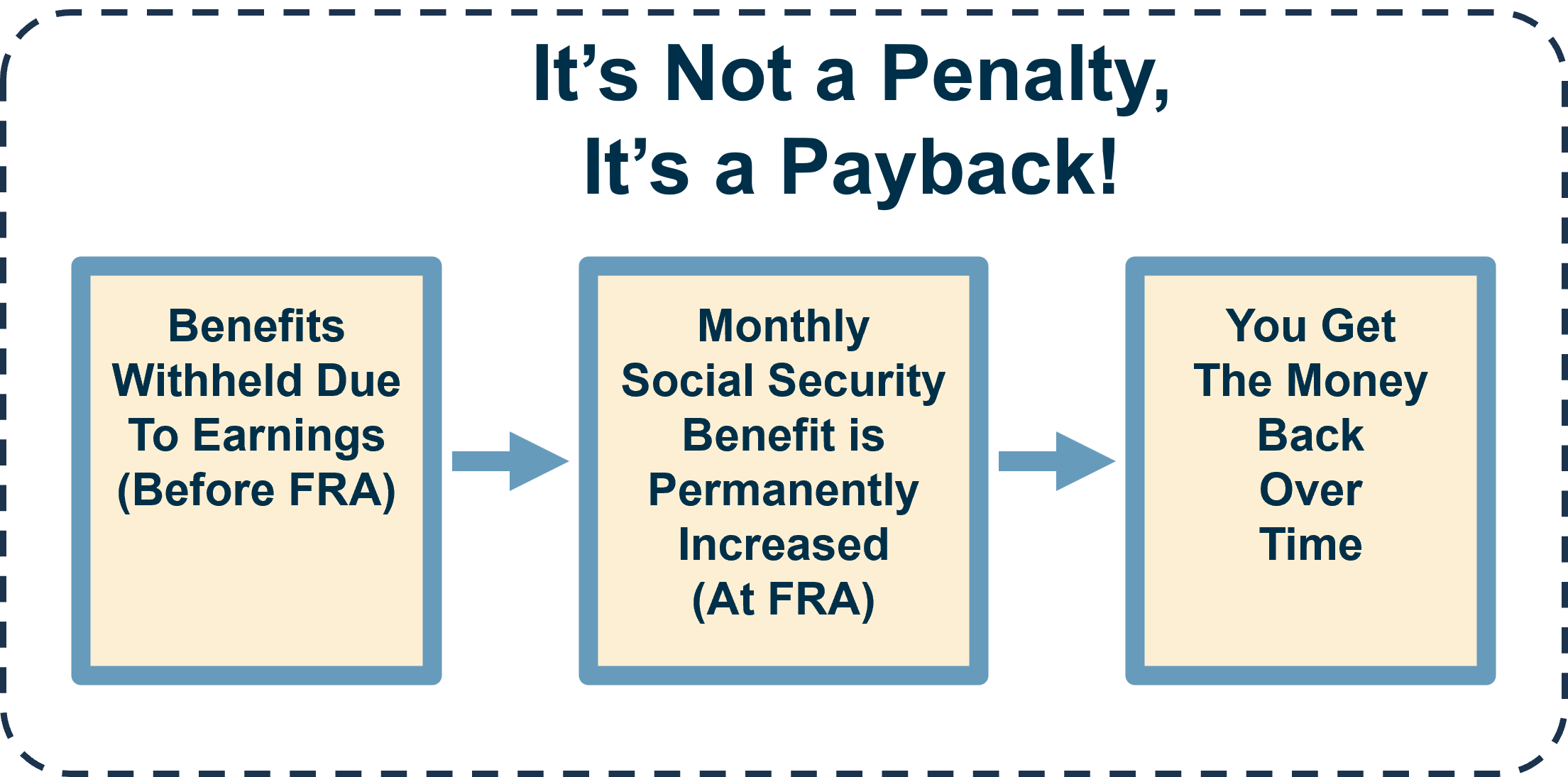

The Big Reveal: You Get the Money Back!

This is, without a doubt, the most important takeaway of this entire article. The money withheld by the earnings test is NOT A TAX. You do not lose it forever. The government is simply holding it for you.

When you reach your Full Retirement Age, the SSA performs a magic trick of sorts. They look at all the months your benefits were withheld and they give you credit for them. They will automatically recalculate your monthly benefit, increasing it slightly to pay you back over your lifetime for the money they held. It's like a forced savings plan that results in a slightly larger check for the rest of your retirement.

Knowing this should completely change how you view the earnings test. It's not a penalty to be feared, but a temporary adjustment to be planned for.

Earnings Test Flowchart

What Kind of Income Counts?

Another common question is what the SSA considers "earnings." The test only applies to money you make from working. This includes:

- Wages from an employer (your gross pay, not your take-home pay).

- Net earnings from self-employment.

Crucially, the test does NOT apply to other sources of retirement income. The following do not count towards the earnings limit:

- Pension payments

- Annuities

- Investment income (interest, dividends, capital gains)

- Withdrawals from your 401(k), IRA, or other retirement accounts

You can have significant income from these sources without triggering the earnings test at all.

Putting It All Together: A Smart Strategy

So, how do you use this information? The earnings test is a major factor in deciding the best time to claim your benefits. If you plan to continue working, the simplest way to avoid the hassle and complexity of the earnings test is to delay claiming Social Security until you reach your Full Retirement Age, or even better, until age 70. By doing so, you not only bypass the test completely, but you also lock in a much larger monthly benefit for life.

Of course, not everyone has that luxury. If you need to work and claim benefits before your FRA to make ends meet, that's perfectly fine! The key is to go into it with your eyes open. Understand the earnings limit for the year, estimate your income, and be prepared for the temporary withholding. Knowing the rule transforms a potential shock into a predictable part of your budget.

The earnings test seems complicated, but at its core, it’s a temporary rule with a fair outcome. By understanding it, you reclaim control and can confidently design the working retirement that’s right for you.